Introduction

Let's take an example of Zoho Company which manufactures beach toys of all shapes and sizes.

These toyss are sold worldwide. We study Zoho Company in this section because of the variety of methods Zoho

uses to pay its employees. Companies usually pay employees weekly, biweekly, semimonthly, or monthly.

How often employers pay employees can affect how employees manage their money.

Some employees prefer a weekly paycheck that spreads the inflow of money.

Employees who have monthly bills may find the twice-a-month or monthly paycheck more convenient.

All employees would like more money to manage. Let's assume you earn $50,000 per year.

The following table shows what you would earn each pay period. Remember that 13 weeks equals one quarter.

Four quarters or 52 weeks equals a year.

We can estimate an annual salary by doubling the full-time hourly rate and then multiplying by 1,000.

Example: $10 an hour, $10 × 2 × 1,000 = $20,000.

You can estimate an hourly full-time rate by dividing an annual salary by 1,000 and then dividing by 2.

Example: $20,000÷ 1,000 = $20; 20÷ 2 = $10.

Now let us look at some pay schedule situations and examples of how Zoho Company calculates its payroll for employees of different pay status.

Hourly Rate of Pay and Calculation of Overtime

The Fair Labor Standards Act sets minimum wage standards and overtime regulations for employees of companies covered by this federal law.

The law provides that employees working for an hourly rate receive Time-and-a-half pay for hours worked in excess of their

regular 40-hour week. Many managerial people, however, are exempt from the time-and-a-half pay for all hours in excess of

a 40-hour week. Other workers may also be exempt. In our example, Zoho Company is calculating the weekly pay of Adam who works

in its manufacturing division.

- For the first 40 hours Ramon works, Zoho calculates his gross pay (earnings before deductions) as follows:

Gross Pay = Hours employee worked × Rate per hour;

- Hourly overtime pay rate = Regular hourly pay rate × 1.5

- Gross pay = Earnings for 40 hours + Earnings at time-and-a-half rate

Hourly Rate of Pay; Calculation of Overtime

| Employee | M | T | W | Th | F | S | Total |

| Adam | 12 | 9.5 | 9 | 9 | 10.75 | 11.25 | 61.5 |

Let's assume that rate is $10.00 per hour.

- Number of overtime hours = 61.5 − 40 = 21.5 hours

- Overtime rate = $10 × 1.5 = $15

- Gross Pay = (40 hours × $10) + (21.5 hours × $15) = 400 + 322.5 = $722.5

Straight Piece Rate Pay

Some companies, especially manufacturers, pay workers according to how much they produce.

Zoho Company pays Mary for the number of toys she produces in a week.

This gives Mary an incentive to make more money by producing more toy's.

Mary receives $1 per toy, less any defective units.

The following formula determines Mary' gross pay:

Gross pay = Number of units produced x Rate per unit

Companies may also pay a guaranteed hourly wage and use a piece rate as a bonus.

However, Zoho uses straight piece rate as wages for some of its employees.

Example: During the last week of March, Mary produced 600 toys. Using the above formula, Zoho Company paid Mary $600.

Differential Pay Schedule

Some of Zoho's employees can earn more than the $1 straight piece rate for every toy they produce.

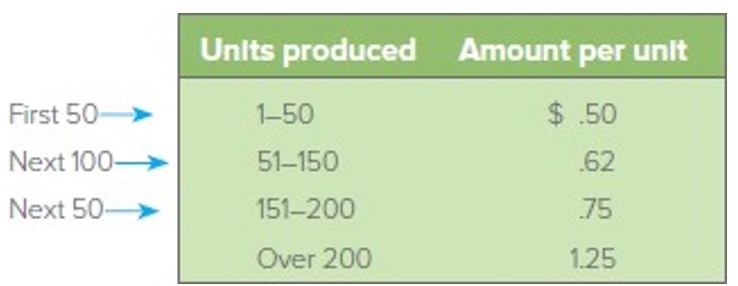

Zoho Company has set up a differential pay schedule for these employees.

The company determines the rate these employees make by the amount of units the employees produce at different levels

of production.

Example: Zoho Company pays Mike on the basis of the following schedule:

Last week Mike produced 300 toys. What is Mike' gross pay?

Answer: (50 x $.50) +(100 x $.62)+(50 x $.75) + (100 x $1.25) = $249.50

Straight Commission with Draw

Companies frequently use straight commission to determine the pay of salespersons.

This commission is usually a certain percentage of the amount the salesperson sells.

An example of one group of companies ceasing to pay commissions is the rental-car companies.

Companies such as Zoho Company allow some of their salespersons to draw against their commission at the beginning of

each month.

A draw is an advance on the salesperson's commission. Zoho subtracts this advance later

from the employee's commission earned based on sales.

When the commission does not equal the draw, the salesperson owes Zoho the difference between the draw and the commission.

So, basically:

- Commission is a certain percentage of the amount a salesperson sells.

- Draw is an advance on the salesperson's commission.

Example: Zoho Company pays Omar a straight commission of 10% on his net sales (net sales are total sales less sales returns).

In June, Omar had net sales of $60,000. Zoho gave Jackie a $500 draw in June. What is Omar's gross pay?

Answer: ($60,000 x .10) − $500 = $6,000 − $600 = $5400

Variable Commission Scale

Zoho Company pays some people in the sales department on a variable commission scale.

A company with a variable commission scale uses different commission rates for different levels of net sales.

Let's look at this case and assuming the employee had no draw.

Example: Last month, Amy's net sales were $150,000. What is Amy's gross pay based on the following schedule?

Variable Commission Scale

| Up to $35,000 | 4% |

| Excess of $35,000 to $50,000 | 6% |

| Over $50,000 | 8% |

Answer: Gross Pay = ($35,000 x .04) + ($15,000 x .06) + ($100,000 x .08) = $1,400 + $900 + $8,000 = $10,300

Salary Plus Commission

Zoho Company pays Henry a $2,000 monthly salary plus a 4% commission for sales over $25,000.

Last month Henry's net sales were $60,000.

Zoho calculated Henry's gross monthly pay as follows:

Answer: $2,000 + ($35,000 x .04) = $,2000 + $1,400 = $3,400

Simple Interest

Calculation of Simple Interest and Maturity Value

- The cost of borrowing money from a bank is called interest.

- The bank charges us interest for using its money to buy things such as cars and properties.

- Likewise, when you deposit money in a bank, the bank pays you interest for the privilege of using your money.

- Interest calculated only on principal is called simple interest and

it is computed as a constant percentage of the money borrowed or invested for a specific time.

- By definition simple interest I equals principal (amount borrowed or invested) multiplied by

the interest rate multiplied by the number of years

.

The formula is: I = Prt

Where,

- I = the amount of simple interest,

- P = principal; capital, amount invested, amount borrowed or sometimes called the present value,

- r = annual simple interest rate,

- t = time in years.

- For t: Months or days need to be converted into years.

- Months to years: divide by 12

- Days to years: EXACT INTEREST divide by 365, ORDINARY INTEREST divide by 360 (also called the Banker’s rule.) If not specified in the question, assume ordinary interest.

Maturity Value

Maturity Value is the final amount that must be repaid in the end,

or the final value of the money you deposited in the bank.

Some synonyms often used are future value or total amount due or S.

Maturity Value (MV) = Principal (P) + Interest (I) which is the amount of the loan (face value) + Cost of borrowing money

It is also expressed as below:

- MV = S = P + I

- MV = S = P + Prt

- MV = S = P(1+rt)

- r = (S − P) ÷ (P × t)

- t = (S − P) ÷ (P × r)

Example

Star Appliances borrowed $20,000 to replace office carpets. The loan was for 6 months at an annual interest rate of 4%.

What are Star's interest and maturity value?

Answer: I = $20,000 × 0.04 × 6 ÷ 12 = $400

MV = $20,000 + $400 = &20,400

Example

Star Appliances borrowed $20,000 to replace office carpets.

The loan was for 1 year at a rate of 4%.

What are Star's interest and maturity value?

Answer: I = $20,000 × 0.04 × 1 = $800

MV = $20,000 + $800 = &20,800

Example: How long does it take for AED 120,000 to grow to AED 210,000 at a simple annual interest rate of 7%?

Round your answer to 2 decimals

Answer: t = (S − P) ÷ Pr = (210,000 #8722 120,000)/120,000 × 0.07 = 10.71 years

Two Methods of Calculating Simple Interest and Maturity Value

Method 1: Exact Interest Used by Federal Reserve banks and the federal government

This method assumes that number of days in a year is 365 days

Time = Exact number of days ÷ 365

Example: On March 4, Amy borrowed $40,000 at 4%. Interest and principal are due on July 6.

Question: Find the interest and mature value

Answer: I = P × R × T = $40,000 × 0.04 × 124 ÷ 365 = $543.56

MV = P + I = $40,000 + $543.56 = $40,543.56

Method 2 : Ordinary Interest (Banker's Rule)

This method assumes that number of days in a year is 360 days

Time = Exact number of days ÷ 360

Example: On March 4, Mary borrowed $40,000 at 4%. Interest and principal are due on July 6.

Question: Find the interest and mature value

Answer: I = P × R × T = $40,000 × 0.04 × 124 ÷ 360 = $551.11

MV = P + I = $40,000 + $551.11 = $40,551.11

Example: Adam paid the bank $23.55 interest at 7.5% for 75 days.

How much did Henry borrow using the ordinary interest method?

Answer: P = I ÷ (Rate × Time) = $23.55 ÷ (0.075 × (75 ÷ 360) = $1,507.20

Interest (I) = Principal (P) × Rate (R) × Time (T)

Check 23.55 = 1,507.20 × 0.075 × (75 ÷ 360)

More exercises

The following formula will used in the next exercises: Interest (I) = Principal (P) x Rate (R) x Time (T); MV = P + I

Exercise 1: Calculate the simple interest and maturity value for the following problem (Round to the nearest cent as needed):

Principal = $8,000; Interest Rate = 3.50%; Time = 20 months;

Answer:

I = $8,000 × 0.035 × (20 ÷ 12) = $466.66;

MV = P + I = $8,000 + $466.66 = $8466.66

Exercise 2: Calculate the simple interest and maturity value using ordinary interest for the following problem (Round to the nearest cent as needed):

Principal = $2,000; Interest Rate = 5%; Date borrowed: March 8; Date repayed: June 9;

Answer:

T = Exact number of days ÷ 360 = 160 − 67 = 93 days;

I = $2,000 × 0.05 × (93 ÷ 360) = $25.83

MV = P + I = $2,000 + $25.83 = $2,025.83

Exercise 3: Use the same data of Exercise 2 and the exact interest to find simple interest and maturity value.

Answer:

T = Exact number of days ÷ 360 = 160 − 67 = 93 days;

I = $2,000 × 0.05 × (93 ÷ 365) = $25.48

MV = P + I = $2,000 + $25.48 = $2,025.48

Exercise 4: Solve for the time in month or years where:

P = $500; Interest rate = 7%; Simple interest = $150.00;

Answer:

T = $150.00 ÷ ($500.00 × 0.07) = 4.28 years

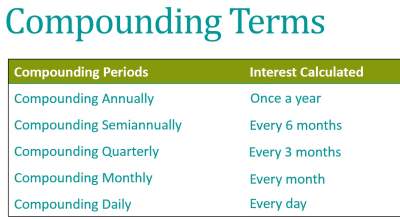

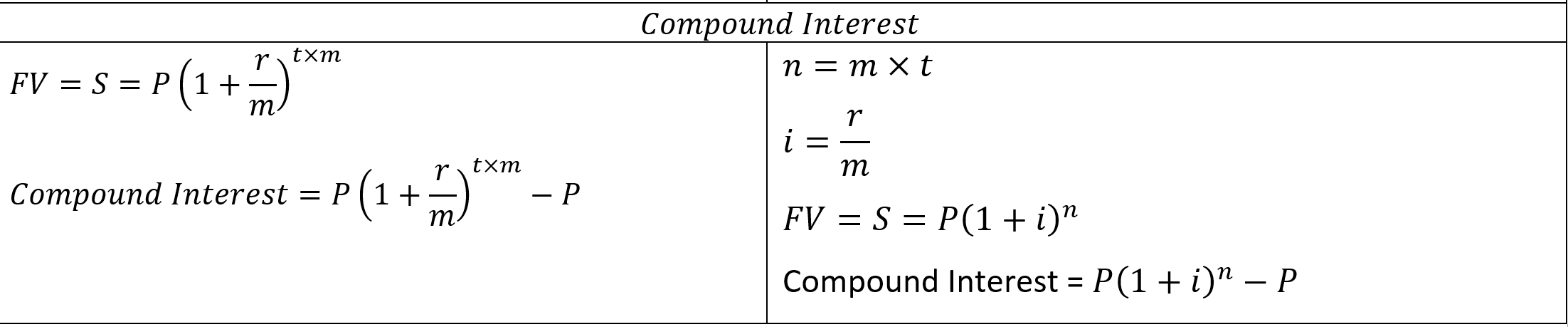

Finding Compound Interest

When the amount of interest earned at the end of the first period is added to the principal

(so both the principal and interest earns interest in the next period),

the interest is said to be compounded.

The sum of the original principal and total interest is called the compound amount or accumulated value.

(or future value or maturity value or S)

The amount of compound interest is the difference between the accumulated value S and the present value P.

Tools for Calculating Compound Interest

Number of periods (N) Number of years multiplied by the number of times the interest is compounded per year

For example, if you compounded $100 for 4 years at 8% annually, semiannually, or quarterly, what is N and R?

Number of periods (N) and Rate for each period (R)

| Period | Rate |

|

| Annually: 4 × 1 = 4 | Annually: 8% ÷ 1 = 8% |

| Semiannually: 4 × 2 = 8 | Semiannually: 8% ÷ 2 = 4% |

| Quaterly: 4 × 4 = 16 | Quaterly: 8% ÷ 4 = 2% |

Simple Versus Compound Interest

Let's look at the example below to illustrate the difference between simple and compound interest:

Simple Interest

Adam deposited $80 in a savings account for 4 years at an annual interest rate of 8%.

Question: What is Adam's simple interest and maturity value?

Answer:

I = P × R × T = $80 × 0.08 × 4 = $25.60

MV = $80 + $25.60 = $105.60

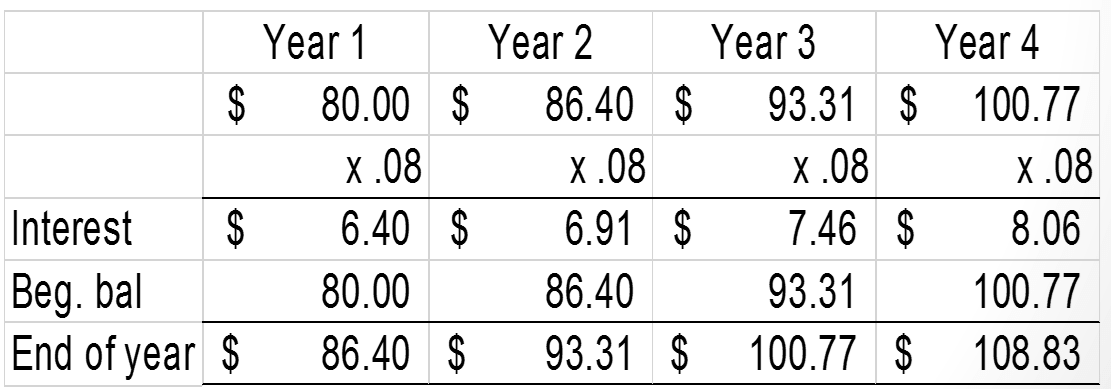

Compound interest

Adam deposited $80 in a savings account for 4 years at an annual interest rate of 8%.

Question: What is Adam's interest and compounded amount?

See the below table that shows how to calculate the compound amount:

Answer: The Interest = $108.83 - $80.00 = $28.83

Finding Compound Interest Manually and by Formula

The following formula are used to compute compound interest manually:

Example: Sami promised his daughter alice that he would give her $8,000 8 years from today for graduating from high school.

Assume money is worth 6% interest compounded semiannually.

Question: What is the present value of this $8,000?

Answer: Using the formula above; where m = 2 (semiannually); t = 8 years; n = m × t = 16 periods; i = 6 ÷ 2 = 0.03; (1+0.03)16=1.6047

FV = S = P (1 + i)n = $8,000. Hence P = $8,000 ÷ 1.6047 = $4,985.35

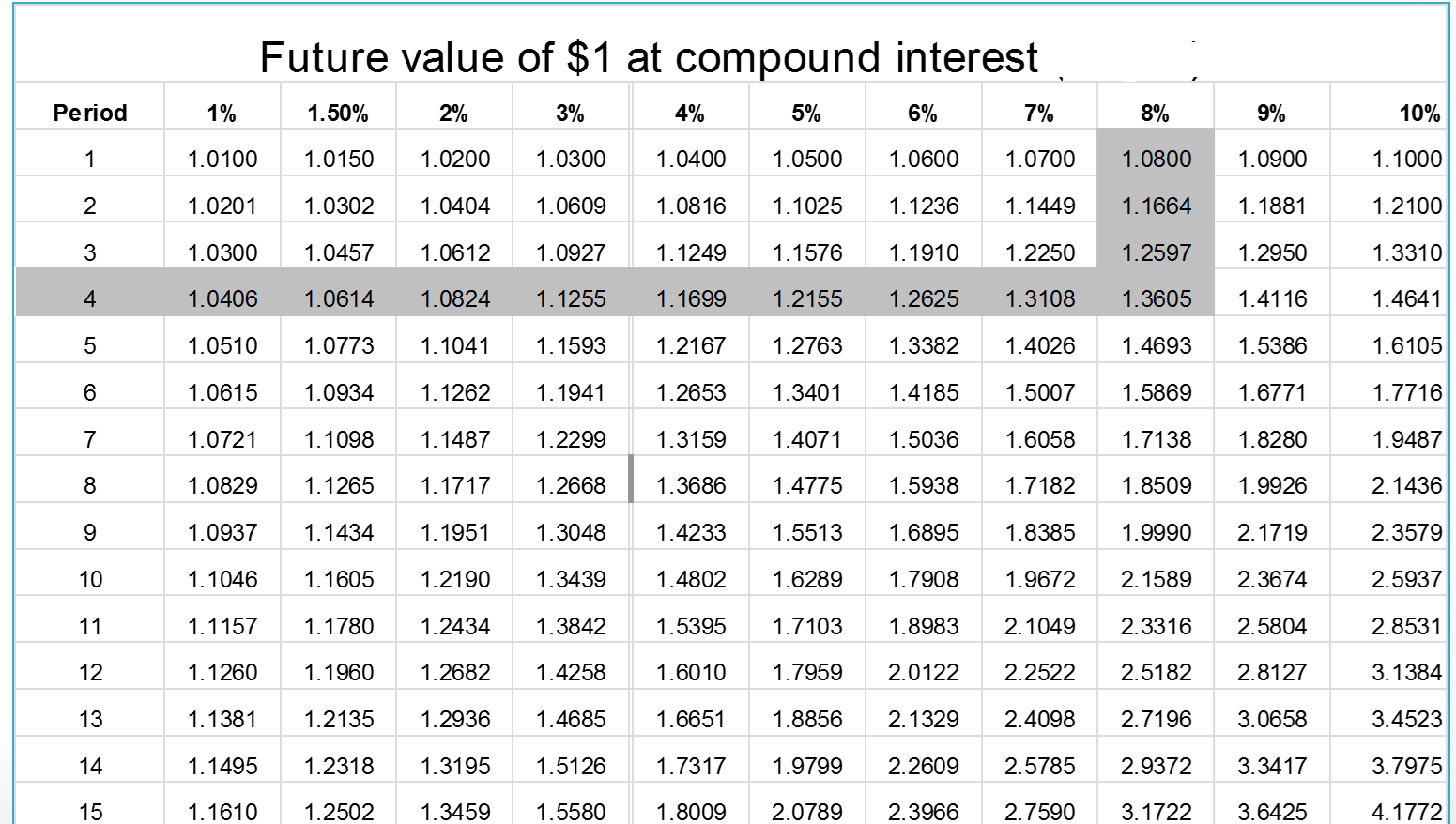

Calculating Compounded Amount by Table Lookup

Table lookup is another method for calculating the compounded amount. The steps are as follows:

- Find the periods: Years multiplied by number of times interest is compounded in 1 year.

- Find the rate: Annual rate divided by number of times interest is compounded in 1 year.

- Go down the period column of the table to the number desired; look across the row to find the rate.

At the intersection is the table factor for the compound amount of $1.

- Multiply the table factor by the original amount. This gives the compound amount.

For example, the future Value of $1 for 4 years at 8%. The Compound Interest is found as highlighted in the table below:

Exercise: Assume that Mike deposits $5,000 in his savings account that pays 8% interest compounded quarterly.

Question: What will be the balance of his account at the end of 7 years?

Answer:

Periods (N) = 4 x 7 = 28; Rate (R) = 8% ÷ 4 = 2%; Table Factor = 1.7138;

Compounded Amount = $5,000 x 1.7138 = $8,569.00;

Exercises and solutions

Exercise 1: Paul, owner of a car rental company, loaned $50,000 to Mike to help him open a startup.

Mike plans to repay Paul at the end of 6 years with 8% interest compounded semiannually.

Question: How much will Paul receive at the end of 6 years?

Answer:

N = 6 years x 2 = 12 periods; rate = 8% &# 247 2 = 4%; Table factor = 1.6010;

Compounded amount = $50,000 × 1.6010 = $80,050; Paul will receive after 6 years $80,050

Exercise 2: Mary Indecision has difficulty deciding whether to put his savings in ABC Bank or Seasons Bank.

ABC offers 8% interest compounded semiannually. Seasons offers 4% interest compounded quarterly.

Mary has $20,000 to invest. She expects to withdraw the money at the end of 5 years.

Question: Which bank should Mary choose?

Answer:

ABC Bank:

N = 5 years x 2 = 10 periods; rate = 8% ÷ 2 = 4%; Table factor (10 periods, 4%) = 1.4802;

Compounded amount = $20,000 × 1.4802 = $29,604; So at the end of 5 years the addtional amount = $29,604 − $20,000 = $9,604

Seasons Bank:

N = 5 years x 4 = 20 periods; rate = % ÷ 2 = 2%; Table factor (20 periods, 2%) = 1.4849;

Compounded amount = $20,000 × 1.4849 = $29,698; So at the end of 5 years the addtional amount = $29,698 − $20,000 = $9,698

Seasons has a slightly better deal than ABC.

Exercise 3: Bob deposited $25,000 in a new savings account at 6% interest compounded semiannually.

At the beginning of year 3, Bob deposits an additional $35,000 at 8% interest compounded semiannually.

At the end of 4 years, what is the balance in Bob's account?

Answer:

N = 2 years × 2 = 4 periods; rate = 8% ÷ 2 = 4%; table factor (4 periods, 4%) = 1.1699; after 2 years compounded amount = $25,000 × 1.1699 = $29,247.5

At the beginning of year 3, Bob deposited additional $35,000. So the new amount in his account would be = $35,000 + $29,247.5 = $64,247.5

At the end of 4 years, the new compounded amount would be = $64,247.5 × 1.1699 = $75,163.15

Exercise 4: Mary deposits $6,000 into an account earning 4% annually.

After 8 years what will Mary''s balance have grown to, including interest?

Answer:

N= 8 years × 1 = 8 periods; rate = 4 ÷ 1 = 4%; table factor (8 periods, 4%) = 1.3686;

Compounded amound = $6,000 x 1.3686 = $8,211.60

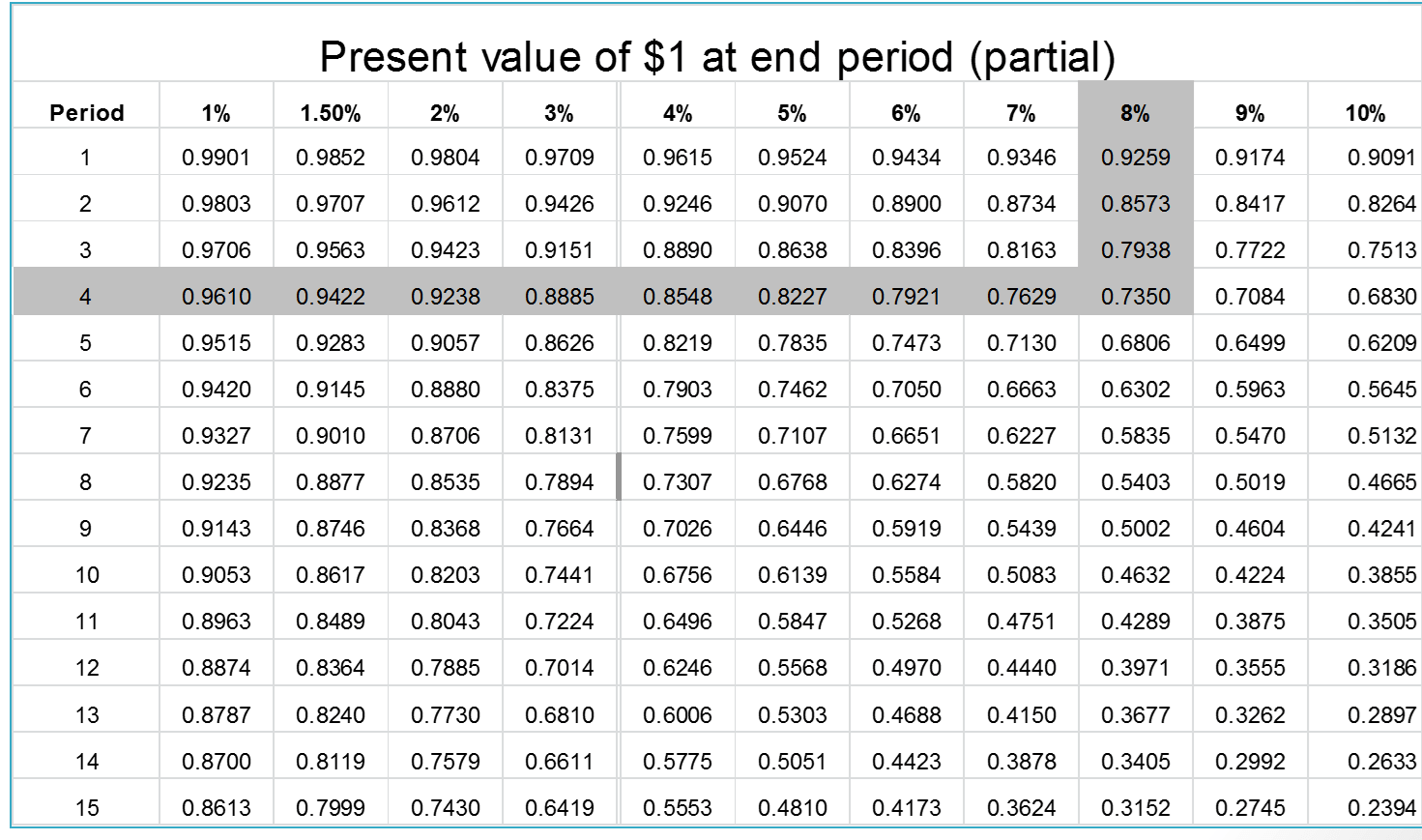

Calculating Present Value by Table Lookup

Here are the steps in calculating the present value by table lookup:

- Find the periods: Years multiplied by number of times interest is compounded in 1 year.

- Find the rate: Annual rate divided by number of times interest is compounded in 1 year.

- Go down the Period column of the table to the number desired; look across the row to find the rate. At the intersection of the two columns is the table factor for the compound value of $1.

- Multiply the table factor by the future value. This is the present value.

Let's use a previous example to computer and compare compounded amount and present value.

Adam deposited $80 in a savings account for 4 years at an annual interest rate of 8%.

Question: What is Adam's future value (compounded amount) and presente value?

Answer:

N = 4 × 1 = 4; R = 8% ÷ 1 = 8%; Table factor for future value (4 periods, 8%)= 1.3605;

Compounded Amount = Present Value × 1.305 = $80 × 1.3605 = $108.84

N = 4 × 1 = 4; R = 8% ÷ 1 = 8%; Present Table factor (4 periods, 8%)= 0.7350;

Present value = Future Value × 0.7350 = $108.84 × 0.7350 = $80

Exercise: Nadia needs $30,000 for college in 4 years. She can earn 6% compounded semiannualy at her bank.

How much must Nadia deposit at the beginning of the year to have $30,000 in 4 years?

Answer:

Periods (N) = 4 x 4 = 16; Rate (R) = 6% ÷ 2 = 3%; Present Table Factor (16 periods, 3%) = 0.7284;

Present value must be: Future value × 0.7284 = $30,000 × 0.7284 = $21,852

Calculating Nominal and Effective Rates (APY) of Interest

Nominal Rate (stated rate) is defined as the rate on which the bank calculates interest.

Effective rate (APY) = Interest rate for 1 year ÷ Principal

Calculating Effective Rate APY

Let's see the two following examples of calculating effective rate APY:

Example 1: 12% compounded quaterly; Principal = $4,000

N = 4 × 1 = 4 periods; Percent = 12% ÷ 4 = 3%; Table factor (4 periods; 3%)=1.1256;

Compounded Amount = $4,000 × 1.1256 = $4,502.40; Interest for 1 year = Compounded Amount - Principal = $4,502.40 - $4,000= $502.40

Effective rate (APY) = $502.40 ÷ $4,000 = 0.1256 = 12.56%

Now, let's see the value of the effective rate (APY) if it's compounded semiannually:

N = 2 × 1 = 2 periods; Percent = 12% ÷ 2 = 6%; Table factor (2 periods; 6%)=1.1236;

Compounded Amount = $4,000 × 1.1236 = $4,494.40; Interest for 1 year = Compounded Amount - Principal = $4,494.40 - $4,000= $494.40

Effective rate (APY) = $494.40 ÷ $4,000 = 0.1236 = 12.36%

For more details, please contact me here.

Date of last modification: March 11, 2019